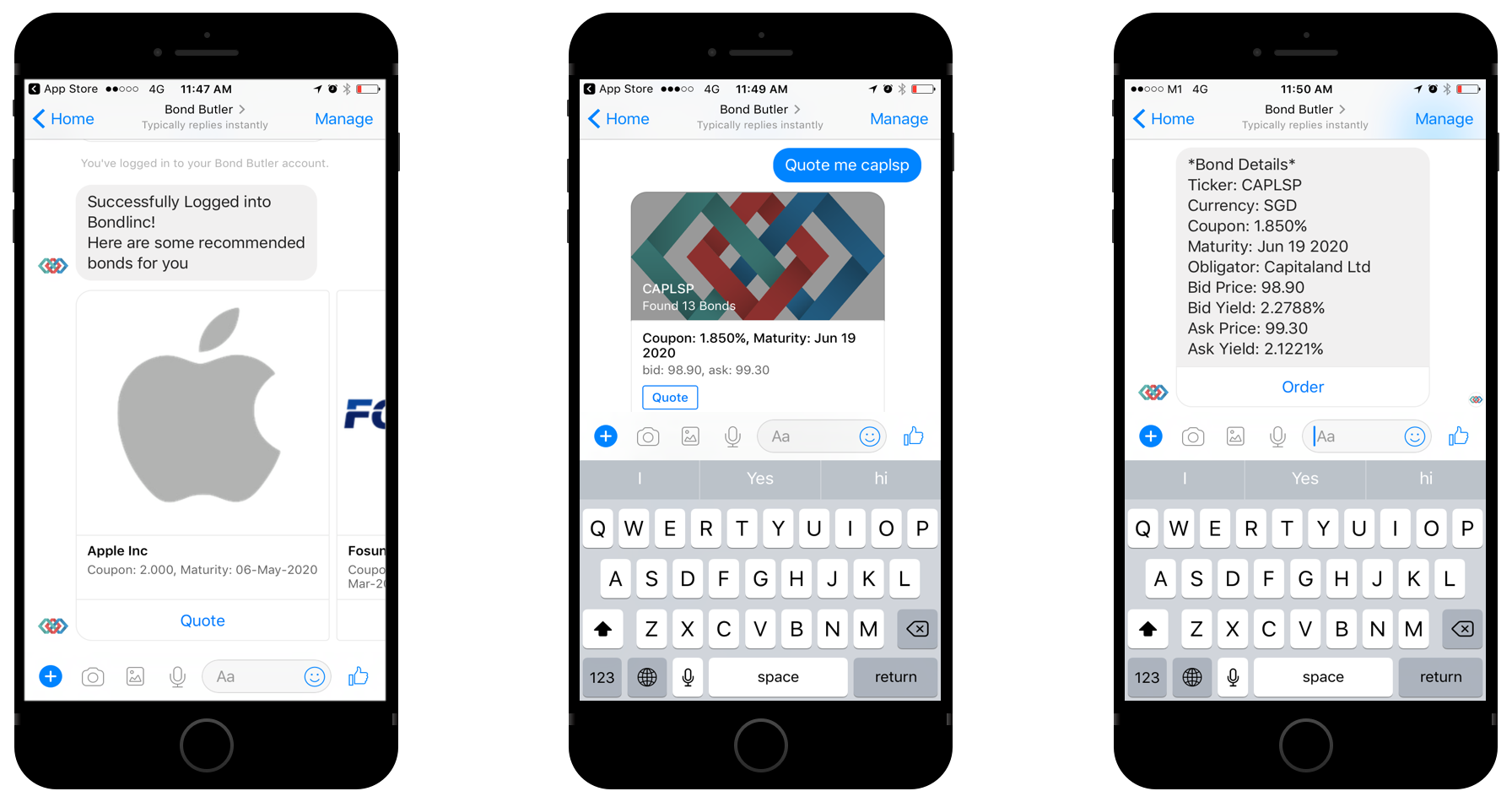

Bondlinc is very honored to be awarded Best Regulation Reporting Solution in Asian Private Banker’s 6th Technology Awards for the fourth consecutive year!

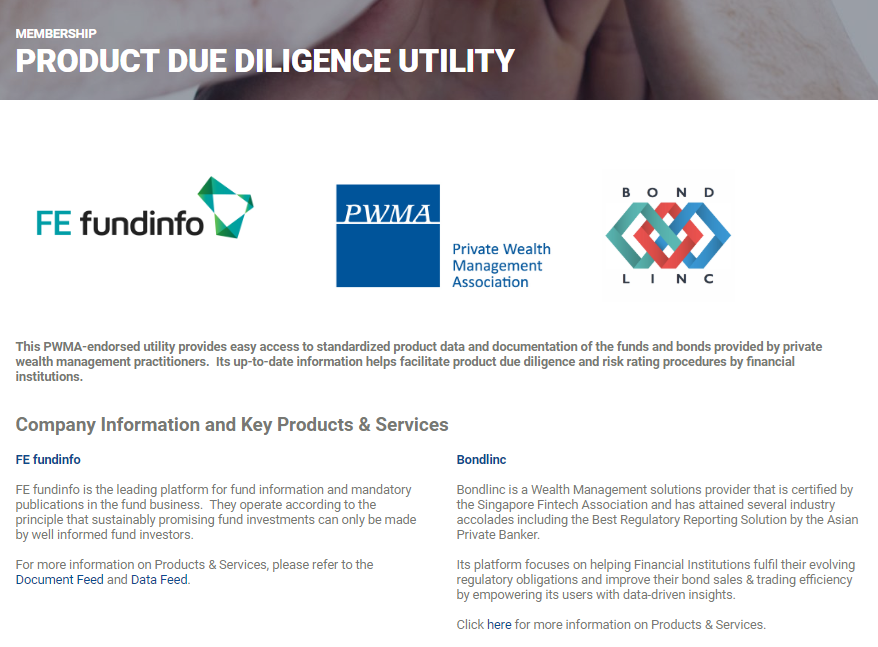

We would like to thank Asian Private Banker for recognising our efforts this past year. In 2020, we launched our Private Wealth Management Association (PWMA) endorsed Product Due Diligence Utility (PDDU) to standardise and simplify Product Due Diligence requirements for Financial Institutions, namely Complex Product requirements, and to ensure an industry-wide streamlined approach is adopted.

The Best Regulation Reporting Solution is awarded to the solution that best enables private banks to provide clear audit trails that adhere to regulators’ standards, and equips private banks with sufficient agility to keep up to date with regulatory changes across multiple jurisdictions.

Technical Indicators of this award category include:

Facilitates compliant record-keeping which could facilitate rapid response to regulators’

Record access requests

Possesses data aggregation, storage, and analytics capabilities

Provides clear audit trails by tracking and recording documentation

Adheres to regulatory standards across different jurisdictions

Creates regulatory reports that are compliant with different regulators’ requirements

A big congratulations to all the winners of this year’s Asian Private Banker Technology Awards!